The post SaaS exit readiness: when should founders start thinking about exiting? appeared first on saas.group.

]]>Based on our experience at saas.group, going from the first acquisition chat to an actual deal may take up to several years. Building with an exit in mind is not something founders often do. But when they start to consider one, it’s usually a mix of personal, financial, and strategic factors, in that order.

Planning for an exit may not be the most exciting task for a founder, but when done right, it can align timing, process, market trends, and personal goals well enough to promise a great exit you truly deserve.

The stages of a SaaS business

SaaS businesses typically move through various stages: startup, growth, maturity, and sometimes decline. Each phase demands a different skill set and presents unique challenges:

- Startup: This phase requires creativity, product development, and finding product–market fit. Many companies are sold at this stage (especially in the AI era), but this is more about opportunism than sustainability. These sales are often driven by private equity firms betting on rapid growth.

- Growth: Scaling operations, building teams, and optimizing systems are critical here. This is no longer the 0-to-1 journey. It’s about adding structure and processes and bringing in specialists instead of generalists. It might be the best time to sell, although it can be the hardest time to let go.

- Maturity: Businesses at this stage focus on maximizing profitability and maintaining steady growth. Many face challenges with efficiency and risk plateauing unless they return to the drawing board to rekindle that growth mindset.

- Decline or plateau: If growth stagnates, it may be time to innovate or explore new markets. Unfortunately, this is often when founders start thinking about selling, which can result in less favorable outcomes with reduced negotiation power and fewer buyer options.

Personal goals and post-acquisition plans

Your personal aspirations should be front and center when thinking about an exit. Of course, considering the future of the team, brand, and your legacy is important, but ultimately, you are the one who has to live with the decision.

- Emotional aspect: Letting go of what is potentially your life’s work is a big deal. The journey from idea to exit takes time, not because the offers aren’t good, but because detaching emotionally is hard. That said, you can find an acquirer like saas.group who will keep you involved in a different role. You may continue working on the product with your team even after the acquisition.

- Future plans: Do you have another project or opportunity lined up? We’ve all seen those LinkedIn posts that go from “just sold my company, heading to a remote island” to “I’m bored and unsure what to do next” within a few weeks. Not saying you need a five-year plan, but giving your next step some thought is wise.

- Financial needs: The bigger the deal, the better, right? Not necessarily. Are you selling to fund a new venture, secure retirement, reach a milestone, or simply to take some chips off the table? Your motivation affects the kind of exit you want. And sometimes, saying yes to the right partner instead of the highest bidder pays off more.

- Work–life balance: If running the business has taken a toll, exiting may help you realign priorities. We’ve worked with founders in this situation at saas.group, and one thing stands out: tell your potential buyer why you’re selling. This builds trust and sets expectations. No one wants to bring on a brilliant founder who’s totally burnt out and counting minutes until the day ends.

Business factors to evaluate before selling your SaaS company

Aside from personal goals, several business-specific factors impact your readiness to exit:

- Valuation: Know your worth. Online calculators are a decent start, but consult an M&A broker or advisor for a realistic valuation. Look for social posts and articles. Some founders are very open about their exits. Just remember that no two exits are the same, and you’ll need to be prepared for deep due diligence.

- Financial health: Keep clean, organized records of revenue, expenses, and growth trends. This makes due diligence far easier. At saas.group, we try to streamline this process and give rough valuations early, but that only works if founders know their numbers and can share them confidently.

- Operational independence: Can your business thrive without you? The more your business runs without your day-to-day involvement, the more attractive it is. Making yourself “redundant” may feel strange, but it’s exactly what buyers want. After all, you’ll be moving on eventually.

- Market conditions: Timing isn’t everything, but it matters. Favorable conditions can increase your sale price. Research recent transactions in your niche and check trend reports from acquirers and M&A brokers. Some founders share a lot about their sales online. Don’t hesitate to reach out and ask questions.

- Growth trends: Buyers want growth. If you’ve plateaued, try to revitalize growth before selling. Exiting at the peak is tough emotionally, but waiting too long can hurt your chances or lower your valuation. If an exit is on the table, maximize your return while momentum is on your side.

The power of saying no

Many founders get approached by buyers when they’re not even looking to sell. That’s a great position to be in. It gives you leverage to say “no,” negotiate better terms, or wait for a more strategic fit.

Optionality, focusing on building a great business without chasing an exit, often leads to better outcomes. But this only works if you actually have the option to say no.

That said, don’t feel pressured to sell. If it’s not the right time, it’s not the right time. Just make sure you communicate clearly and respectfully without burning bridges.

Post-sale considerations

The work doesn’t stop when the deal closes. In many ways, it’s just the beginning, for the team, anyway. As a founder, you should be aware of what happens next, especially if there’s an earnout or if you’re staying on in some capacity.

- Onboarding new leadership: Document your workflows and key processes. If there’s no clear successor in your company, the acquirer will need to install someone quickly. Make their transition as smooth as possible.

- Team alignment: Changes can be hard for your team. Even though many buyers advise against announcing the deal too early, you should still plan how to handle that communication. Transparency earns trust. When done right, it sets the new owner up for success.

- Tech stack integration: Yes, change is painful but only in the short term. Consolidating tools helps teams operate efficiently and feel more connected. It also makes operations smoother and cheaper in the long run.

Final thoughts

Preparing for a SaaS exit is a challenge that requires foresight, planning, and a clear understanding of both personal and business objectives. By thinking through your own goals, assessing business health, and staying flexible, you can set yourself up for a smoother, more rewarding transition.

Whether you’re months or years away from an exit, the best time to start preparing is now. And doing it with the right partner may even make the whole experience, dare we say, enjoyable.

The post SaaS exit readiness: when should founders start thinking about exiting? appeared first on saas.group.

]]>The post Inside saas.group: how we built a home for profitable SaaS businesses appeared first on saas.group.

]]>What’s your personal story?

I’m Tim Schumacher, and I’m one of the founders of saas.group. We acquire and grow small to medium-sized SaaS (Software as a Service) companies. Our primary customers are actually the SaaS businesses themselves – we buy them, improve them, and scale them up.

What makes saas.group unique is our focus on the “middle market”. We’re not chasing unicorns or trying to build the next big thing from scratch. Instead, we look for solid, profitable SaaS businesses that are often overlooked or ignored by larger investors. These are typically companies doing anywhere from $2M to $10M in annual recurring revenue.

We are also very proud of being founder-friendly. That means we really try to accommodate every possible scenario a founder has for their exit. If the goal is to cash out and move on to the next product or just start spending more time with family, we don’t want to tie these people down with earnouts and make them stay with us even though they’re miserable. At the same time, if a founder feels like they’d like to still be growing their business with us with access to more resources and the help of a great community, we will draft the terms to make sure we work together successfully for the years to come.

We focus on a sustainable approach for saas.group, as we do for all of our businesses, and always keep an eye on where we stand according to the Rule of 40%. That means we’re balancing our companies’ growth vs profitability so that the sum is always around 40%. For some companies that means 20/20 ratio and for some 10/30 or even 5/35 makes a lot more sense. It keeps our priorities straight and emphasises the long-term goals.

How did you come up with your business idea?

The idea for saas.group evolved from a combination of experiences and observations. I’ve been investing for a while after my own exit from Sedo.com and always enjoyed the process. I was putting the money into companies I truly believed in. But with angel investments, you have a very limited say in what is actually happening there. I wanted to be more hands-on, to really steer these businesses towards success. At this moment I already knew I wasn’t a 0-to-1 kind of founder but rather enjoyed taking solid working businesses to the next level, bringing the operations up to speed, and finding potential for optimizing.

My “aha” moment really came when I received a proposal from a broker to acquire a SaaS business for just 4X EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). This valuation seemed extremely reasonable, especially when compared to the sky-high multiples you see for public SaaS companies or even real estate investments.

That’s when it clicked. There was this whole world of smaller SaaS businesses that weren’t getting attention from big investors or private equity firms. They were too small for most institutional investors, but too big for individual entrepreneurs to easily acquire. This gap in the market presented a huge opportunity.

I realized I could combine my desire to be more hands-on with the opportunity to acquire these undervalued SaaS businesses. This would allow me to actively help grow these companies while also creating significant value through adding resources and applying my own personal experience.

To validate the idea, I dug deeper into the market for smaller SaaS acquisitions. I looked at broker listings, talked to founders who were considering selling, and analyzed the financials of various SaaS businesses. Everything I found confirmed that there was indeed a gap to be filled in this space.

My experience building and growing my own companies and investing played out pretty well here. I’d previously co-founded and sold Sedo.com, one of the largest domain marketplaces. This experience gave me a deep understanding of how to scale internet businesses, which was directly applicable to growing SaaS companies.

After the initial validation, I decided to take the plunge and start saas.group. But I knew I didn’t want to do it alone. I reached out to some trusted contacts in my network, including folks I had worked with before. That’s how I ended up with Ulrich, at first. We’ve worked together on Sedo, knew how to communicate with each other, and had really complementary skill sets. I knew that I’d be comfortable going at it with him.

We then did an early friends and family investment round to get things off the ground. This was crucial not just for the capital, but also for bringing in some key team members. Tobias was one of the investors from this round and he later ended up joining us full-time.

There are hundreds of stories where companies failed because of the wrong co-founder dynamics and we are very lucky to nail down our core competencies, bring different strengths to the table, and also have spent quite a bit of time in SaaS already to put our egos aside to make this work.

It’s crucial to have the right people when you have a big vision. I’m happy to say that at this moment with saas.group, the team that we’ve brought together is really something I’m deeply proud of.

What were the first steps starting saas.group?

The first concrete step was acquiring the first SaaS business. This was DeployBot, a continuous deployment tool for developers. I bought it for about $1 million, which I financed with my own money from the Sedo exit.

From day one, DeployBot was bringing in about $50,000 in monthly revenue. As I was working with an agency at the time, about half of that went to development and hosting costs, leaving me with a 50% profit margin. This margin was crucial as it allowed us to start paying back the acquisition cost immediately. Which doesn’t often happen in SaaS. It was really a revelation for me that a SaaS company could start bringing the returns right after I “started” it.

The next steps involved improving DeployBot’s operations. The focus was on reducing churn, improving the product, and optimizing marketing. At the same time, I started looking for the next acquisition.

I then repeated this process, acquiring more SaaS businesses like Juicer, Prerender, and ScraperAPI.

It’s important to note that not every acquisition worked out perfectly. For example, we ended up selling Sniply after it didn’t perform as we had hoped.

We ended up selling it to the best possible buyer (and one of Sniply’s oldest customers) whom we believed could still do a much better job than we did. The idea for saas.group, however, is to buy and hold the businesses indefinitely. I prefer to stay positive but realistic in this situation, again given my angel investment experience. These things happen and sometimes even the best teams can’t take the product to the next level.

This taught us valuable lessons about what to look for in potential acquisitions.

Our business model has stayed fairly consistent throughout this process: acquire undervalued SaaS businesses, improve their operations, use profits to pay back acquisition costs, and grow the businesses. Unlike venture-backed startups, we need to focus on profitability from day one, not just growth at all costs.

It’s definitely been harder than I initially thought, particularly in terms of integrating different company cultures and technologies. But it’s also been incredibly satisfying to see these businesses grow and thrive under our management. It’s a continuous learning process for the entire team. We end up buying businesses with very different setups, tech stacks, and team sizes. Staying true to what we believe in and having a very strong thesis about every business we buy definitely helps but we also want to be flexible with the terms for the founders I mentioned before and make sure teams that join us see the value of the group as soon as possible.

How did you ‘launch’ the business?

To be honest, we didn’t have a big, flashy “launch” moment for saas.group. Our approach was much more focused and targeted. Instead of making a big public announcement, we concentrated on reaching out directly to potential sellers and brokers in the SaaS space.

We started by leveraging my existing network. I reached out to founders I knew who might be considering an exit, as well as to brokers who specialize in SaaS businesses. We also started actively monitoring various marketplaces and forums where SaaS businesses are bought and sold.

Our first “sale” was really our first acquisition – DeployBot. I already had some experience buying businesses during my time in Sedo, so in a way, I knew what to expect but it still taught us a lot about evaluating SaaS businesses, the importance of thorough due diligence, and how to structure deals.

The response to our entry into the market was generally positive. Many founders were excited to have another potential buyer in the space, especially one who understood the unique challenges of running a SaaS business. To this day, the importance of builders selling to builders is something founders mention in our conversations. There’s certain trust about working with people who’ve been there and done that over giving a company away to purely financial institutions.

Another key lesson we learned from this soft launch was the importance of building relationships in the SaaS community. We found that many of our best deals came through word-of-mouth referrals from founders we had previously worked with. And we encourage every founder we talk to about a potential acquisition to reach out to the companies we’ve already acquired. We’re very open and honest about the way we work but having a conversation with somebody who’s been through the process can add a lot more clarity. I always say if your potential acquirer doesn’t introduce you to someone they’ve already worked with before, consider it a pretty bright red flag.

For the first couple of acquisitions, we didn’t even have a website for saas.group. We put together something very simple (and not very pretty) but good enough to explain our model and what we were looking for in potential acquisitions. It served as our calling card in the early days, helping us to establish credibility with brokers and potential sellers.

We made sure to highlight our experience in the tech industry and our hands-on approach to growing businesses.

Over time, we’ve expanded and improved our web presence quite a bit with a strong social media presence, our own podcast, events, and keynote appearances at major SaaS conferences, but that first simple site played a key role in getting us off the ground.

How has saas.group been growing since then?

Our growth has primarily come through continuing to acquire new SaaS businesses and improving their operations. We’ve now done this about 20 times.

In terms of specific tactics, we’ve found that a data-driven approach works best. We’re big believers in the 80/20 rule – focusing on the things that really move the needle. For each business we acquire, we dive deep into the metrics, looking at things like customer acquisition cost, lifetime value, churn rate, and expansion revenue.

We then experiment with different strategies to improve these metrics. This might involve tweaking the pricing model, improving the onboarding process, or investing in customer success. We try a lot of things, measure them rigorously, and aren’t shy about stopping experiments that aren’t working.

For example, with one of our businesses, we found that improving the onboarding process led to a significant decrease in churn. We then doubled down on this, investing more resources into creating a smoother, more user-friendly onboarding experience.

There’s definitely no one-size-fits-all kind of strategy or a playbook that we use, instead, we apply different strategies to each individual SaaS business we acquire, tailoring our approach to their specific market and customer base.

For all the founders out there, I’d recommend focusing on execution rather than trying to come up with a completely unique idea. In my experience, once you start working on an idea, you’ll quickly realize there are already competitors doing something similar. What matters is how well you execute and whether you can do things better than others in your space.

I’d also advise entrepreneurs to embrace experimentation and continuous improvement. Try a lot of things, measure them rigorously, and don’t be afraid to stop initiatives that aren’t working. Then, when you find something that works, scale it aggressively. It’s a simple concept, but it’s amazing how many businesses fail to follow this iterative approach.

The post Inside saas.group: how we built a home for profitable SaaS businesses appeared first on saas.group.

]]>The post The SaaS exit gap appeared first on saas.group.

]]>But first, some eye-opening statistics

- Male-founded businesses in the Technology, Media, and Telecommunications (TMT) sectors, which include SaaS, are valued 1.5 times higher on average than female-founded businesses (Forbes, 2024).

- For every $1 million a female founder receives during an exit, a male founder receives $1.5 million for a similar business, reflecting a 50% disparity in exit outcomes (The Big Exit, 2024).

- Less than 1% of businesses that sold a majority stake were female-founded. In the U.S., this figure was 1.37%, while in Europe and the rest of the world, it was as low as 0.35% (Forbes, 2024).

- Despite the valuation gap, female-founded companies tend to exit faster, with a median time to exit of 7.2 years compared to 8.1 years for all startups (PitchBook, 2023).

Understanding the exit gap

What does “ exit gap” actually mean? It refers to the disparity in financial outcomes when businesses founded by women are sold or exited compared to those founded by men. We all have seen news and reports about great differences in funding and biases in the investment environment for early-stage female-led businesses. But it turns out, it drags on for the entire lifecycle of those companies. And it’s especially visible in SaaS. So, how do we make sure SaaS is less of a bro-land and is more inclusive with equal opportunities for all?

“When I started in this space ten years ago, it wasn’t common to see women in the C-suite, especially at companies going through an acquisition. Though it’s becoming more typical, it’s still not the norm. There has been progress. More women are stepping into leadership roles, and more female-founded SaaS companies are gaining traction, but the gap is still there. M&A has long relied on established networks and pattern recognition, which tend to favor founders and teams that resemble those who have exited before. Unless those systems are rethought, the outcomes stay the same.That said, some acquirers are taking more deliberate steps. I’ve seen more diversity on deal teams, which brings broader perspectives to how opportunities are evaluated. There’s also been a shift in sourcing. More firms are proactively building relationships with underrepresented founders instead of relying on traditional channels. A number of private equity firms have also introduced internal diversity benchmarks and are tracking representation within their portfolios. It’s not yet consistent across the industry, but the direction is encouraging.

I’m also seeing more women in senior roles on the buy side, both at private equity firms and strategic acquirers. More women are leading deals and influencing decisions. On the founder side, more women are building strong companies and getting in-market. Many are creating opportunities for others through hiring, mentorship, or expanding access. The change is gradual, but it’s real and becoming harder to ignore.”

© Diamond Innabi, Software Equity Group

What causes the exit gap in the first place?

Let’s be real, it is probably a wild mix of biases, barriers, and behaviors that have been forming for years, and we can’t manage to shake off. But it’s also the fact that there are way fewer women in tech overall. If the percentage of female-led businesses is already so low, seeing those exit numbers kind of makes sense. Yet, it’s important to understand each of the factors to get an idea of how to fight them.

1. Systemic undervaluation of female-founded businesses

According to some of the recent reports, female-founded businesses don’t get the valuations they deserve compared to pretty much identical (we’re talking early-stage here) ideas coming from their fellow male entrepreneurs. Getting back to that upsetting statistic of women exiting their businesses earlier, there might be a question of the stability and longevity of the ventures. And here we seem to enter the chicken and the egg situation of either it is less money for female-led businesses or fewer businesses due to the lack of support.

2. Access to capital

Female founders face significant challenges in accessing venture capital (VC) funding. In 2025, woman-founded startups received just 2.3% of all VC funding (Marketing Scoop, 2025).

3. Bias in investor networks

The investment ecosystem remains predominantly male-dominated, with fewer female investors and decision-makers. This lack of diversity just makes it harder to make the decisions that even in 2025 seem to be too bold to be true, therefore allowing the decision-makers to fall for the “traditional” patterns.

“M&A still has an old-school culture, made up mostly of men. Anecdotally, I can tell you that most M&A advisors are men. Most buyers are firms led by men. And most of the voices giving advice about M&A are male. That means women are less likely to have a friend or two who can offer casual advice through the sale process. One of our goals at They Got Acquired is to create a space where all founders, not just women, can learn about how to sell their business in a really accessible way. And my hope is that by leading this brand with a female voice, women might be more likely to ask us for support. I do a lot of free calls with founders who want to sell their business, and many of them are women. In that way, I see us as playing a tiny part in helping to close the exit gap.”

© Alexis Grant @They Got Acquired

Consequences of the exit gap

The shortsightedness of the investors and acquirers whose decisions are driven by biases and ancient societal attitudes is pretty remarkable. Not only does it install additional barriers for incredible talent to create beautiful products, teams, and cultures, but it also has direct implications for the entire industry and, therefore, the economy at large.

It’s not just about the missed opportunities for investors here, but also slowing down the progress toward gender diversity in tech.

We always talk about the importance of letting SaaS customers know the product is for them, they can relate to it, and see the unique benefits for themselves. And if founding a SaaS was a product, getting any woman to subscribe would be a pretty big challenge.

How do we bridge the exit gap?

First of all, it’s important to emphasise that bridging the gap is definitely not about favors. It’s not about deliberately hiring women or investing in female-owned businesses to make the numbers work. It’s about creating equal opportunities and an environment where all the amazing businesses and people get the same treatment. It’s going beyond gender towards a non-subjective assessment of the idea, metrics, and overall relevancy of the business.

1. Increasing female representation in investment/acquiring companies

It’s true that you feel more comfortable talking to a person who at least looks a bit more like you. They may not have the exact same experience, but they can relate. The M&A scene is highly male-driven, and having a female representative there may make all the difference for founders who have already been fighting the “it’s raining men” situation throughout their career, to also have to defend their “baby” in the same environment. This is not to say working with male M&A experts and advisors immediately puts women in a less favorable position, but to emphasise the opportunity to have a smoother, less stressful process.

2. Providing mentorship and support

The exit gap has been given more and more visibility lately. There’re quite a few support groups and experienced advisors who can help with guidance now.

We, at saas.group, always encourage founders we approach to talk to anybody who has sold to us before. And yes, we have to admit (sadly), we have never acquired a company that was female-led (and are working hard to make sure that changes), but we do have incredible women CEOs who know exactly how it works from the inside. And let’s face it, that’s really what matters after the acquisition.

“Ask every question: Many times, women feel afraid to ask “what exactly does this term mean”, for fear that they will look dumb or unknowledgeable. But the reality is, most of us didn’t start businesses because we had an in-depth knowledge of M&A. It’s very important to read every detail of the deal, and stop and understand what each piece actually means.

Ignore “valuations”: You know what your business is worth? Whatever someone will pay for it. This works in both ways– if you have something great that someone really wants for a strategic reason, they’ll blow past the multiples. If you have a business that is in a category that has super high valuations, but you’re almost out of cash and no one wants it, the multiples are completely irrelevant. Multiples are a guide, not a mandate, and folks who get stuck on how an offer compares to multiples in the market often are the ones who don’t get a deal done.

Make sure your income is RED. I know, we are used to keeping income in the BLACK. But when I say RED, I mean Recurring, Expected, and Diversified. Not all revenue is created equal, and strengthening your revenue will definitely help your valuation.

Revenue is vanity, profit is sanity. Build a good, profitable business, and acquirers will be interested. Sure, there are tech companies that sell for huge numbers that aren’t profitable. But they are few and far between, and they sure as hell aren’t female-founded.

And finally, talk to women who’ve done it before!”

© Carrie Kerpen @Whisperer Group

3. Taking action

Yes, there are a few more great initiatives that governments, banks, and holdings could implement to help bridge that gap. But it’s also about taking those opportunities. It’s not just the top-down approach. Visibility won’t happen without people who want to be visible.

Having women on stages and in publications creates great waves. And it doesn’t have to be big. You don’t have to become Taylor Swift of SaaS to be celebrated. Building in public, sharing little hacks, putting your efforts out there for everyone (to judge, yes, there’s this side, too) but also to inspire, could make the world of difference.

At some events/podcasts/stages, you’ll still be the only woman. But so what? Seeing you there may inspire a couple of others to join, and that’s where it all starts.

Conclusion

The exit gap is real, and it’s a reminder of all the biases and barriers that the entrepreneurial ecosystem has been prone to for years and can’t shake off. Yet, there are already some visible shifts that are moving the tech industry to become a more inclusive space. That means investors taking action, acquirers establishing more sustainable processes and creating a safer environment for a conversation, and advisors building healthier ecosystems. It’s still a long way to go, but by addressing the root causes and implementing targeted solutions, we might just shape the landscape that, at the end of the day, benefits all.

The post The SaaS exit gap appeared first on saas.group.

]]>The post saas.group brings more exciting SaaS deals for Black Friday 2024 campaign appeared first on saas.group.

]]>Inside, you’ll find exclusive discounts on a wide range of SaaS software, including marketing, sales, development, SEO, and CRM tools.

Here’s a preview of some brands that will reveal exclusive Black Friday deals:

Rewardful, Affiliate Program Software

Rewardful is affiliate management software that’s simple. If offers deep integrations, including with Stripe.

Tower, Git Client for Mac and Windows

Tower is a native Git client designed for Mac and Windows. It is loved for its ease of use and powerful features.

ScraperAPI, Data Collection Tool

ScraperAPI is a complete data collection tool that enables businesses to collect public information at scale. Users, including Gabriel M. and Arun K., praise its effectiveness in overcoming challenges related to programmatic requests.

Juicer, Social Media Aggregator

Juicer is a social media aggregator used for its user-friendly interface and seamless integration. They’re gearing up for a Black Friday deal that promises to enhance online presence.

Pipeline CRM, CRM for Salespeople

Pipeline CRM is a sales CRM platform built for salespeople. It’s designed to improve sales operations and communication within teams.

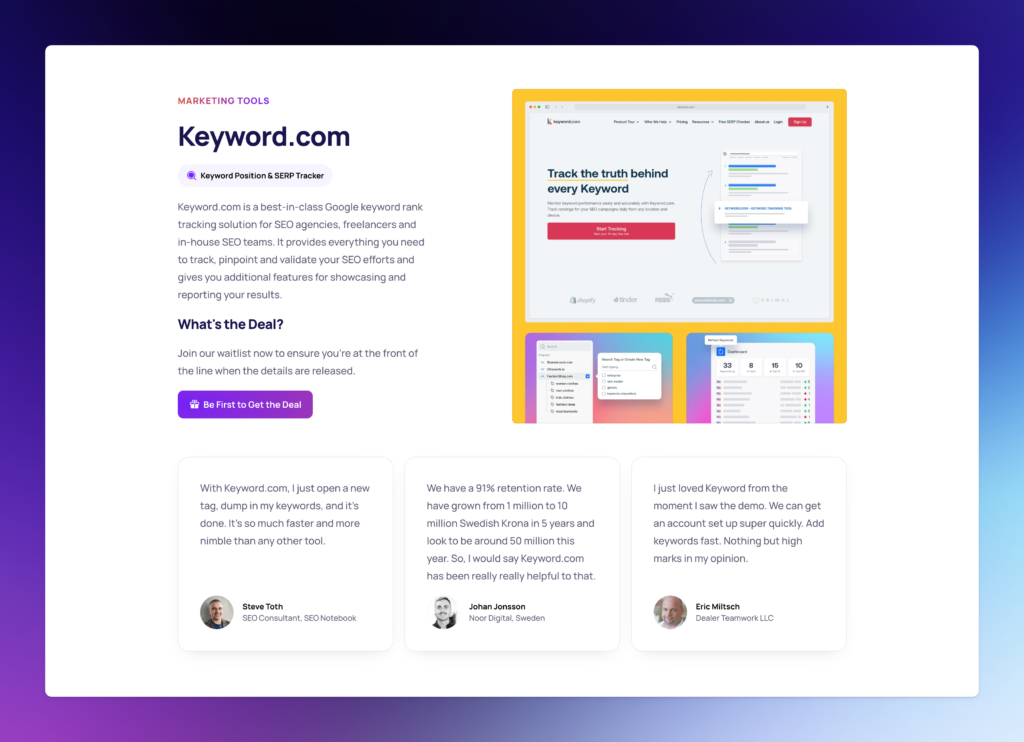

Keyword.com, Keyword Position and SERP Tracker

Keyword.com is a SERP and keyword rank-tracking solution. It is appreciated for its speed and efficiency in keyword tracking.

Beekast, Collaborative Tool

Beekast is an online collaborative solution widely adopted for it its simplicity and reliability in making events more interactive.

DeployHQ, Code Deployment Tool

DeployHQ is a tool to deploy your websites from Git, SVN and Mercurial repositories to your very own servers.

Seobility, All-In-One SEO Software

Seobility is an all-in-one SEO tool praised for its powerful features and ease of use in website optimization.

MyWorks, eCommerce Accounting Automation

MyWorks is a powerful integration between e-commerce and accounting platforms, appreciated for its time-saving features and seamless synchronization.

AddSearch, Site Search Solution

AddSearch is a lightning fast fully-featured accurate site search solutions platform with a customizable design.

zenloop, Customer Experience Management Platform

zenloop, a CXM platform to create easy AI-powered surveys for satisfaction measurement, NPS, and beyond.

Don’t miss your deal!

Join the waitlist to be the first to access these and many more deals once they’re live.

The post saas.group brings more exciting SaaS deals for Black Friday 2024 campaign appeared first on saas.group.

]]>The post SaaS M&A: buyer due diligence appeared first on saas.group.

]]>Ideally, you want someone who is not only ready to pay the most but also someone who understands what you’re building and shares the vision for the company to take it to the next level. There are some key considerations when selling your startup, including important questions to ask potential acquirers and red flags to watch out for.

The main question is, of course, what you, the founder, want from the acquisition.

Everyone is talking about getting a “dream exit,” but not all dreams are equal.

For some founders, the primary goal is to sell quickly, easily, and for the highest price. However, many are serious about keeping the legacy alive and making sure the team and the customers are still happy and cared for. Whatever it is for you, it’s good to get this covered before you begin the sales process.

Once this is clear, you can start preparing for the acquisition. And some do it from day one, which is a great idea. The more work you put into it at the beginning, the easier it will be to make sense of it all for the potential acquirer and then the final transition. It’s all about streamlining your operations, making sure that your financials are clean, and building honest and trustworthy relationships with your acquirers.

Acquisitions take time. No matter how founder-friendly or fast the process is, it’s a lot of laying the groundwork for the other team to take over. And if you do it right, it can be smooth sailing, and you’ll be way better positioned to get what you want from the acquisition.

But due diligence goes both ways.

All founders are conscious of the things acquirers are going to ask them. However, it’s also important to know what you can (and should) ask them.

Questions to ask your potential acquirer:

- What is your track record with acquisitions? Are you known for successful integrations and positive outcomes, or do you have a history of struggling to make acquisitions work?

- What is your vision for the future of the products we offer? Will our product be integrated into your existing offerings, or will it remain separate? What does your roadmap look like for the future?

- What will happen to our team after the acquisition? Will they be retained, and if so, what will their roles be? Will there be changes to our company’s culture, management structure, or other aspects?

- How will the acquisition impact our existing customers and users? Will they be migrated to your platform? How will you communicate any changes to our customers and users?

- What is the valuation and deal structure of the acquisition? What percentage of the sale will be cash vs. stock, and what are the terms of any earn-out or performance-based incentives? What will happen to any outstanding equity or stock options held by our employees?

It’s important to remember that an acquisition doesn’t end once the money hits your bank account. You may still need to collaborate and help with the transition, so ensuring open and honest communication from the start is key.

Red flags to watch out for during the acquisition:

1. Lack of cultural fit: If the potential acquirer has a culture that clashes with yours, it could lead to a difficult integration and potentially result in losing your best team players.

2. Unrealistic valuation: If the potential acquirer is offering a valuation that seems too good to be true, it probably is. It could be a sign that they are not taking into account all the factors that determine your company’s true value.

On the one hand, it could seem good for you. More money? Good! But that could also mean they haven’t assessed all of the relevant factors and, probably, aren’t taking this seriously enough. It could also indicate that there is a hidden agenda and that an unrealistic offer serves as a distraction from the true intentions.

It’s understandable, though, getting a huge valuation is flattering. Someone sees your company as a really valuable asset. But when approached with such, try to be realistic and research the deals companies similar to yours have had, the state of the market, and your financials. It might not be the easiest to stay on top of these things, but it may save you from an unfavorable outcome in the long run.

3. Lack of clarity on the buyer’s intentions: If the potential acquirer is vague about their plans for your company after the acquisition, it could be a sign that they are not fully committed to the deal.

4. Weak financials or track record: If the potential acquirer has a history of financial instability or has a weak track record of successfully integrating acquired companies, it could be a sign to go into this cautiously.

5. Lack of compatibility with your goals: If the potential acquirer’s goals for the company do not align with your goals, it could lead to a difficult integration and potentially damage the business in the long run. Having a clear understanding of their goals and if they align with your vision for the company is extremely important if you care where it’ll go after you leave.

Selling your company is a major decision that requires careful consideration and planning. It’s important to be clear about your goals and what you want from the acquisition and to prepare well in advance to increase your chances of success. Asking the right questions and being aware of potential red flags when evaluating potential acquirers can help ensure that you find the right buyer who shares your vision for the company and can take it to the next level.

The post SaaS M&A: buyer due diligence appeared first on saas.group.

]]>The post How to value my SaaS business appeared first on saas.group.

]]>The truth is it’s your business performance that determines the multiple.

There are a few valuation methods:

- SDE-based* – usually the smaller deals, <$1M ARR

- ARR-based** – more applicable for rapidly growing companies

- EBITDA-based*** – steady growth / profit ratio, >$2M ARR

SDE* or Seller’s Discretionary Earnings – a measure of the earnings of a business and is the most common measure of cash flow used to value a small business.

ARR multiple** – a SaaS company’s market valuation to its Annual Recurring Revenue (ARR).

EBITDA multiple*** – formula comparing the enterprise value of a business to its annual earnings before interest, taxes, depreciation, and amortization.

According to the most recent report by acquire.com (Jan 2024), SaaS startups got acquired on the marketplace at a 4.3x TTM profit multiple. Some go for as little as 0.63x and others as much as 34x TTM profit (where TTM profit was greater than $1,000).

Bear in mind that deals done on marketplaces tend to be smaller, with acquirers focusing on the growth potential of the business. “Boring” businesses in the space that don’t experience rapid growth but rather focus on sustainable profitability in our experience tend to go at anything between 1x and 10x.

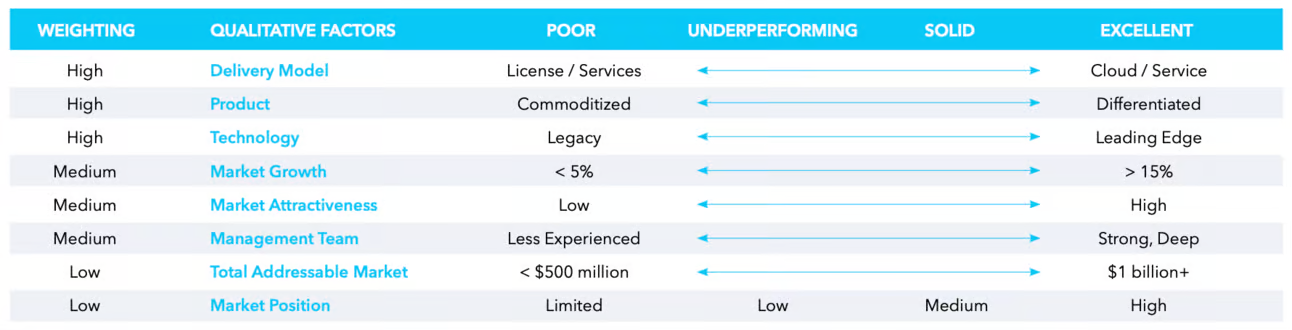

There are quite a few numbers between 1 and 10, though. So how to determine where your business valuation could fall? Let’s start with the quantitative factors that affect it. Here’s a great rundown from Software Equity Group:

To oversimplify it, you can try to place your business within this chart and assuming the poor performers would be offered anywhere from 1 to 1.5X, underperformers – 1.5 to 3X, solids – 3 to 6, and top of the class could expect it to be from 6 to 10X, you’d be getting a VERY rough estimation of your possible multiple.

While the numbers matter a great deal, to quote Pavel Prokofiev, Head of M&A at saas.group – “SaaS valuation is not a science, it’s an art”. So there are a few qualitative factors to take into account, too.

Here’s what SEG (Software Equity Group) suggests to consider:

We would definitely add churn rate, growth trajectory, dependency on the founder brand, culture, and whether or not the company is bootstrapped or funded to these charts. Here’s why:

- Churn. A metric that keeps founders awake at night. It gives potential acquirers an idea of the sustainability of your business, future growth trajectories, and potential risks associated with slower customer acquisition. The benchmark for b2b SaaS is 7% annually. Anything below puts you in the “desirable” basket, anything higher potentially affects your valuation negatively.

There are of course exceptions for younger companies that do not necessarily have a massive existing customer base and therefore churn of new customers have a bigger impact on the overall churn, but if a product is very sticky and showing high switching cost once implemented and used for several months/years, the churn might always improve, even if the business doesn’t change. Obviously, the younger a company, the more volatile the overall churn rate might look like. - Growth trajectory. You want to sell your company when acquirers can still see the potential to go bigger, faster, and stronger. Having the potential to acquire more customers, win more markets, and expand into new geographical areas is something acquirers would prefer any day. It might be psychologically difficult to let go of a business that does exceptionally well but on the other hand, stagnant or even declining growth trajectory may result in lower multiples for the seller, more stress during the negotiations, and a way longer selling process overall.

- Dependency on the founder brand. Having a strong founder brand associated with the company can be both a blessing and a curse. Depending on the exit strategy, an acquirer can greatly benefit from having the founder on board. They are the visionary, the bridge between the company and its key customers, and someone who can make the transition easier for all parties involved.

On the other hand, if customer loyalty is primarily tied to the founder, their departure could lead to significant customer loss. Founders should keep this in mind while building their companies. While a personal brand can be a tremendous asset, over-reliance on it might become a hidden risk. - Culture. Or better yet, culture alignment. Getting your SaaS company acquired means giving the business and its team a new home. And everyone wants to end up in a loving, respectful, and fun home, don’t they? So making sure acquisition doesn’t mean stripping you down of all your values and processes is a big deal. Yes, there’s pretty much no way nothing’s going to change but ensuring a smooth transition and respect for your setup and values is essential for building long-lasting relationships.

- Bootstrapped VS funded. The never-ending battle. Obviously, acquiring a bootstrapped company is just easier. Less names on your cap table, fewer obligations, and in general usually a smoother and faster deal. Now, of course, neither of the setups is the ultimate right one for all. It’s simply something to take into consideration when you’re selling your business. How will the deal work for you? Who gets the liquidity preference? Do founders get paid at all? This may not only affect the exit strategy but also add to the overall stress of the situation. So before considering your exit, we’d recommend clearing it all up with your investors to make sure everyone is on the same page and understanding the outcomes.

Valuing your SaaS business is both an art and a science. Understanding the quantitative factors like ARR, LTV to CAC, and revenue retention rates provides a foundation, but don’t overlook the qualitative aspects that significantly impact your valuation. Metrics such as churn rate, growth trajectory, and dependency on the founder’s brand play crucial roles in determining how attractive your business is to potential acquirers.

Ultimately, planning for your valuation should be a strategic part of your business growth. Buyers are looking for more than just numbers—they seek sustainable growth and a profitable future. By understanding these dynamics and preparing accordingly, you can position your SaaS business for a successful exit that benefits all stakeholders involved.

The post How to value my SaaS business appeared first on saas.group.

]]>The post 5 steps to sell your SaaS business appeared first on saas.group.

]]>Decide why you want to sell

This is the step that isn’t discussed much. Who cares, right? Your numbers are good and there’s still a lot of potential to grow. Why would anyone want to know that you’ve burned out and would rather work on a different product that you got excited about?

Well, acquirers care. Most of us do, anyway. Some of the reasons to sell the business we hear the most about are:

- Taking chips off the table. Having all your eggs in one basket might feel a little intimidating. And the desire to diversify and invest in other assets is a very valid reason to start looking for an acquirer of your business.

- Retiring. As simple as that. You’ve had an awesome run with your company, you’re proud of the legacy you’ve built and now it’s time to spend time with family, take that year-long vacation you’ve dreamt of, or simply garden. And if you’d rather be growing tomatoes instead of going through a 2-year earnout period, your acquirer would want to know that to offer the fastest exit possible.

- Not seeing a way to grow. The next big win is right around the corner but you don’t really have the resources or expertise to take it to the next level. This is perfect grounds for a long-term partnership with a company that has exactly what you’re looking for and has already worked with similar cases. This way, founders may even find it the most beneficial to stay with the buyer after the acquisition to work on their beloved product and be able to learn how to scale it further.

- You’re a starter, not a scaler. We all have different sets of skills and granted, anything can be learned, maybe it’s just not what you’re looking for at the moment. You love the grind and creating something out of nothing. Would you be happy staying with the acquirer long-term realizing that? No one is interested in having a person miserable at their job, so having this information helps your buyer come up with an exit strategy that matches your goals.

Prepare your business for sale:

- Ensure the best valuation

- Get your financials and documentation in order

- Address legal requirements

- Have data room ready

- Work on transferability

Culture fit, efficient deal-making, and clear communication are great but it’s usually the price that matters the most. And there are a few things you can take care of prior to the acquisition to ensure getting the best return on your years invested in business.

Metrics that affect SaaS business valuation are Monthly/Annual Recurring Revenue, Net Revenue Retention, LTV to CAC ratio (lifetime customer value to the cost of acquisition), TAM (Total Addressable Market), and YoY Growth Rate.

Bear in mind that even after getting all the numbers, each business is evaluated individually taking into account its unique position on the market, dependability on the founder’s brand, strengths and weaknesses, and much more.

Ensure you protect your intellectual property from the outset to maintain your competitive edge and steer clear from potential consequences for both you and your business.

Focus on reducing churn and truly understand your customers by providing opportunities to leave feedback and communicate proactively with you. Improve your customers’ onboarding and overall experience to turn them into ambassadors and promoters.

Your differentiation strategy matters! Tech rarely allows you to stand out in the competition, at least not for long. So finding what makes your business unique and positioning it strategically can increase your chances for good valuation.

Having all this information in the data room helps your potential acquirer get a good understanding of your situation in a timely manner and see potential ways to grow your business further. If at the same time you’ve also been working on making sure you’re no longer crucial for the day-to-day operation of your business, it’s a big green flag for the buyer. Transferability is important. If it’s the founder who’s been working on the vision, product development, and customer support 18 hours a day for the past 4 years and it’s only them who have all the bits and pieces together neatly stacked inside their head, well, the odds of the business falling apart after they’re gone increase dramatically. And no acquirer out there wants to figure out how to make it work without that one and only stakeholder.

Find the right buyer: ensure cultural fit, do buyer due diligence

Who wouldn’t want to buy a business like yours? You’ve put all the blood, sweat, and tears into making it great, so getting the right buyer shouldn’t be a problem. Well, this is only partially true. Even if you’ve got all the leverage and your numbers are amazing, figuring out the right fit is no small deed.

Are you selling to a strategic buyer in hopes to get the highest valuation? And being featured on TechCrunch as “acquired by Google (Microsoft/NVIDIA/ your option)” doesn’t sound too shabby either? Take a look at the biggest players in your space, prepare your undeniable offer, and go for it.

Do PEs look like a good fit? Yes, maybe a big influx of cash is exactly what your business needs to become the rocketship it was always supposed to be. It might be hard to work with that kind of growth, and the economic situation doesn’t suggest the fastest returns on this strategy. But hey, what is life if not a big gamble?

How about those programmatic acquirers and holdcos like saas.group? Run by SaaS operators who opt for more sustainable growth and slower but steadier returns. Might not be the most exciting ride but it is a great opportunity to see your product and team go further. And since deal-making is what they do on a daily basis, you can expect the easiest and fastest acquisition process of all.

Now that we have gone through some of the types of acquirers, how do you determine the fit? One thing we always suggest at this stage is checking out the previous deals. Numbers, terms, times, whatever you can find. Connect with the founders who sold to this buyer already, what are they saying? Website testimonials are great but having a 1-1 with the person gives you a totally different perspective. And an opportunity for your gut to speak, too.

Check out their social media and podcast/interview appearances. You can usually get a pretty good idea of the company culture and determine whether or not you’d be comfortable speaking/working with these people. Doesn’t give you the most in-depth knowledge but works great for the first vibe check.

Prepare your alignment/misalignment sheet. You’ve figured out what your dream exit looks like, right? Now based on the previous deals your potential acquirer had, what falls under your idea of a dream? And what is something you can absolutely not look past?

Due diligence: financial, tech, legal, HR

Due diligence is a meticulous process where you’ll be asked for all kinds of information, and have to dig up contracts you didn’t expect to see ever again with the potential to give you a couple of micro heart attacks because of yet another skeleton in your closet you forgot about.

Here’s a list of what buyers tend to ask for:

- financial statements

- customer contracts

- growth projections

- intellectual property documentation,

and any other relevant information that will demonstrate the potential of your business.

Make sure you go at it with a cold head, lots of patience, and a good lawyer. And not just your second cousin who’s been helping you create your Terms and Conditions page. Find an M&A lawyer who’s been doing similar deals and knows what acquisitions are about. Ask your network for a potential introduction or then again make use of platforms like DueDilio and similar ones.

Even the fastest due diligence takes time. It requires a fast reaction to make sure you’re addressing all the issues that may come up. So at that point, if you haven’t made yourself redundant for your team and day-to-day operations, you’re in for a wild ride. One of the things that’s being assessed during the due diligence is the business’s ability to operate without you, so (turning on the broken record here again) taking care of its independence and transferability is something to consider early on.

Figure out the steps for a post-acquisition process

Did you think the process was over once you signed the papers? Well, with all honesty, that might not even be the middle of it.

Every M&A deal starts with a good intention. Yet, failure to integrate a business remains one of the top reasons for the acquisitions to fail. Hopefully, you’ve been able to discuss the terms of your integrations with your buyer even before you started the selling process but if not, there are still a few things to do to help this.

First of all, it’s all about people. If the diligence process was a lot about your data and metrics, this part of the process is between human beings. So, transparency matters!

Make sure all the steps are explicit instead of implied. Create a plan together with the integration leader. Your expectations and desires should be (honored, yes) first of all, heard.

It starts with leadership and ends with leadership but there are a lot of people in between and getting the information through to them is important. Even the least invasive acquisition process means change. Layoffs, product roadmap alterations, communication with the customers, processes, and culture, expect at least some level of adjustment on all fronts. And it’s not to be rushed because rush creates hassle and hassle usually makes messiness and mistakes. So, hopefully, both you and your acquirer have the listen-first mindset to be able to hear out the points of the other party and act on them.

How does post-acquisition integration work at saas.group?

- No big scary rebrand – we always keep the name and the identity of the company intact.

- No stripping apart the organization into a functional model – every brand remains standalone with its unique processes. Although lately, we’re working more towards introducing more unified tools for the teams, we’re also mindful of the processes they have established over the years.

- Generally, no forcing square pegs into round holes! – if we buy a company, we trust that the founders and the team know the way they operate best. They’ve come this far to be successful and ultimately attractive for us to welcome into the family. So, why change fundamental things? We act as advisors but never push a specific agenda onto our brands.

saas.group‘s approach to post-merger integration stands out for its commitment to founder-friendliness and brand autonomy. By preserving the unique identity of each acquired company, and acting as custodians rather than imposing directives, we aim to support brands in their natural trajectory while offering valuable advice for optimization. By minimizing disruption for both founders and their teams, we try to ensure the most positive experience for all.

Navigating the acquisition process can be complex, but it becomes a way less scary adventure with the right preparation and understanding. By knowing why you want to sell, preparing your business for the process, finding the right buyer, and ensuring clear collaboration for a smooth post-acquisition process, you can achieve your dream exit.

If our values speak to you and resonate with how you do business, get in touch. Discuss your options with our M&A team: Dirk (dirk@saas.group) or Pavel (pavel@saas.group). Learn more about how we grow acquired brands on our blog and podcast pages.

The post 5 steps to sell your SaaS business appeared first on saas.group.

]]>The post Where to sell my SaaS company? appeared first on saas.group.

]]>Let’s start with the why. You should always start with the why. There are no wrong answers here, too, but there’s only 1 right one. And it’s right for you and your particular situation. It’s also the first question we, at saas.group, ask founders who approach us for a possible acquisition.

And the reason it’s so important is because it will affect the way we structure the deal to make sure it makes sense for you.

Structuring the Deal: Aligning with Your Goals

Are you selling to get some chips off the table? You’ve gotten your company this far and now since the growth plateaued, you don’t know what to do, don’t have the resources, or frankly just aren’t sure you’re the right person to take it further. You love to code, design, or talk to your customers. Admin work and hiring are not your cup of tea. Understandable and oh, so very common. In this case, staying with us after the sale is a great option that we can offer you. We get an incredible advantage of having a founder on board who knows all the ins and outs of the product and company. You get more time with something you love until you figure out the next step.

Burned out and can’t wait to leave? Sadly, also something we see often. And hey, we pride ourselves on offering some of the shortest due diligence and sales periods out there. We won’t strap you to a chair and ask you to stay for “just a couple of years longer”. Nobody will feel good about that. That said, being left without a visionary isn’t the best-case scenario for us and may affect the valuation slightly, but you pick your battles.

The earlier a potential acquirer figures out your desires and intentions for the future, the easier it is to craft an offer that actually makes sense. In another case, there can be a complete mismatch that can result in frustrations and lost trust, time, and profits. So when you visualize your dream exit, remember it’s not only about dreaming, it’s also about being realistic about your wants and likes and communicating them transparently with your buyer.

Navigating the Exit Process

The next question is how. How involved do you want to be in the process? Are you ready to dig into research and buyer due diligence and then prepare all the documents for the deal? Or would you rather have someone who’s been through it a few times help you, take over the representation of the business, and eventually make the deal happen?

Acquisitions take time, patience, and meticulous planning. For smaller businesses, the disruption can be so huge, they lose their grasp on the operations, and in case the deal falls through, have to scramble to survive.

In figuring out the how, you should understand the exit structure that makes sense for you (and your co-founders), the taxes and what you’ll be left with after all the deductions, the earnout period, and what you’re getting at the end (cash, stocks, etc.), how your product is going to be affected, and where will your team will end up after the closing.

It seems like a lot to do. And in all honesty, it is. So sometimes it’s better to go through a broker. It’s always better to go through a lawyer. And an M&A lawyer at that. None of the “he’s been helping with my cousin’s divorce” kind of situation. They may have been able to get the alimony right, but keeping an eye on a child and figuring out the company’s future are 2 very different fishes to fry.

Choosing the Right Buyer for your SaaS company

Once you’ve made your piece with the reason you’re selling the company in the first place and how you want to do it, it’s time for the “where”.

We’ll go backwards from here. If in the previous question, your answer was, I want to spend the least amount of time and get the most money, try listing on marketplaces. There are several great, well-respected ones where you get a great volume of potential acquirers eager to learn more about your company. The competition is huge, so you can expect lots of bidding, calls, and a great deal of feedback. That said, also expect a lot of tire-kickers, funds with no funds, and having to dig your way through to find a real fit.

A few options out there:

Flippa.com

If you’d like to have a more tailored approach where the fit is most likely to happen but again not sure if you got the time to do your own research, go with a broker. Yes, the commission is high but you get what you’re paying for: you save time, and get a chance to keep on running the company while somebody else is trying to sell it for the biggest buck possible.

Something to keep in mind is the possible disadvantage of not being the one to represent your business, truly show its value, and build a relationship with the buyer first-hand.

If that’s too big of a concern and you actually have the time to research, do buyer due diligence, and have the introduction calls, go alone. It may take much longer but will give you an advantage of really nailing down the best options for you, building relationships, and living that dream exit dream.

Ensuring a Smooth Transition

And here we come full circle to the why. It is your North Star metric when talking to potential acquirers. Once you have a list of buyers that would make sense for the business, be very transparent with what you want (and what is a big no-no). Buyers appreciate honesty and would be thankful for someone saying 1x on EBITDA and firing the team is not what they’re looking for on the first call, rather than 4 weeks of polite maybes only to ditch them anyway.

Look around, and see what is out there on the website, companies on the portfolio, and LinkedIn content of the acquirer (and those they acquired). Have a few calls with the founders who went through the process with that company. Is their testimonial a true one or in all honesty, they wouldn’t want to go through a process like that ever again?

Check out your biggest clients. What is the chance it would make sense for them to acquire you? We’ve seen a few of those deals going exceptionally well resulting not only in big returns but also in the best possible product development opportunities and team growth.

Make your job a little easier. If you aren’t sure how to approach somebody you’ve worked with or an individual company you think could be a good fit, check out serial acquirers.

They’re always on the lookout for the best deals out there and are happy to take a look at your offer. Obviously, going to each and every one doesn’t make sense in this case either. Do your homework and contact those with similar companies in their portfolio, the knowledge and growth opportunities that would make sense for your exit plan, and those that just feel right.

Here are some examples:

Noosa Labs – for bootstrapped SaaS with $150-$800k in ARR

Enduring Ventures – for “blue collar” companies with $2M ARR 50% gross margins and 20% or greater operating margins

Embrace – mission-critical vertical software, with revenues ranging from $2 – $30M

And, of course, saas.group – for $1-$10M ARR profitable B2B SaaS companies with bootstrapper mindset

There you have it. Before jumping to the most obvious (and the easiest) question of all, figure out the reason to sell and how you see the process go from searching for a potential buyer to after you get all the money in your bank account.

Here is the advice from Tim Schumacher:

“I think I would recommend to really do your due diligence on the buyer.

Really find out who those people are. Are you comfortable with them? Do reference calls with other founders. It’s one thing we always offer at saas.group. You can call any of the 20 founders from whom we bought the business. And you should!

This is a trust thing. And at the end of the day, you’re selling what you’ve put all your life into for the past couple of years.

You want your team to have a good home. You want your customers to have a good home. You want to be there in five years and have this company on your LinkedIn profile. And when you click on it, you don’t want to go to a 404 page. You want to have this business thriving.

It makes you proud as a founder if your company continues on. And that’s how we’re acquiring companies at saas.group. We want the founders to continue to be proud of their businesses 5-10 years later. We preserve the name, we preserve what made the company strong in the first place.

We’re also operators. We’re not treating the businesses as spreadsheets. We’re really treating the businesses as sustainable, great businesses, and growing them further. “

If our values speak to you and resonate with how you do business, get in touch. Discuss your options with our M&A team: Dirk (dirk@saas.group) or Pavel (pavel@saas.group). Learn more about how we grow acquired brands on our blog and podcast pages.

The post Where to sell my SaaS company? appeared first on saas.group.

]]>The post Building a centralized customer support system at saas.group appeared first on saas.group.

]]>That’s why one of the goals of saas.group for 2024 is to implement a state-of-the-art horizontal layer of centralized support. Maria Herrell, the Head of Customer Support at saas.group, heading the development of the support system, offers some insights on the overall customer support strategy and the advantages of having it centralized for our brands.

- The Head of Customer Support is a new role at saas.group that has never existed before. Could you talk a bit about the goal for that role and your main responsibilities?

At the point in 2022 when saas.group acquired us, I was the manager of Pipeline CRM’s customer support team. Pipeline CRM was one of the more mature brands that had been acquired at that point, and so I think what was seen was that our customer support processes were well established, contributing to a high level of satisfaction and efficient resolutions for our customers.

Later, I was asked to take a look and see what could be done on the customer support side for all teams at saas.group. Saas.group’s board thought that a centralized support system could make a great resource for all the new brands entering the group, with a focus on prioritizing collaboration, and knowledge sharing, and truly help everyone grow and reach the goals that we’ve set for ourselves as an organization.

- How do we define great customer support at saas.group?

I would say that great customer support is being responsive to our customers, listening, acting on feedback, and resolving issues as quickly as we can so that our customers can get back to work growing their businesses. That is the reason that they’ve come to our tools, right? Great customer support is having brand knowledge and really understanding the problems our customers face, but also being open to hearing (and sharing internally) the feedback that the people using our product every day have to share.

- What are the benefits of a customer-centric customer service strategy?

When you prioritize your customers, you can compete with even the largest tools out there. We have pretty small teams, and a lot of our competitors have larger teams and hefty resources. Being customer-centric allows us to be impactful and grow relationships with our customers, and contribute to their success. Our team’s objectives are to be knowledgeable, and resourceful, identify opportunities for enhancing our product/service, and make sure that we keep up the collaboration across the brand to be the best we can.

- Do you have a hack, a tip, or a piece of advice for small teams? Like you said, a lot of our brands and, overall a lot of bootstrapped brands in SaaS are very small teams competing with giant companies. When your customer support team is sometimes just a founder, how to stay in control?

First I would take a look at the volumes that you’re encountering and try to understand what’s driving them. Where do they land? Is it product knowledge?

Especially now with all the AI tools, there are so many things that you can put into place to help people find the answers on their own and hopefully become confident users of your product, but also to reduce that need for somebody to look into a ticket every time.

Then, you can reserve those volumes that you’re handling for actual issues that may need to be escalated within your team. What I also noticed on the customer support front is that things are shifting a bit and that people want to be able to find the answer, if possible, without having to reach out and call support.

You still want to be reachable by your customers and be hands-on with things that require attention, but if there’s a way to anticipate common questions and provide resources in these areas, you give people the opportunity to help themselves, and that is an ideal setup for a small team.

- With the addition of the central support team, what’s important for you when you hire people for those roles?

For me, number one would be a cultural match. Does that person share the vision of the organization? Do they agree that having accountability and ownership of their work is important and just understand the team mentality?

When you’re part of a small team, everyone needs to be able to trust and count on each other to contribute.

The second would be being resourceful. No is often the easiest answer, and sometimes it’s the only one, really. But it’s also not the most helpful one. And it doesn’t feel good to try and get something done as a customer and get no for an answer.

So I think having resourcefulness and the ability to offer an alternative solution or work around the problem is incredibly useful in customer support and something that users appreciate.

I would also say kindness. You definitely want somebody who’s a great teammate and builds the culture of your team, as well as who is kind to your customers and demonstrates your company’s values in their interactions.

That’s the combination that I would be looking for in the team.

- You already mentioned that we operate in small teams and brands continue to be independent after they join saas.group, but we do encourage knowledge sharing.

And now you’re building a centralized horizontal layer of customer support. So what are the benefits of it? We have different products with different maturity levels and teams. How does it work in terms of dynamics inside all the brands?

When you join saas.group, you get access to the central team and all the shared experiences. You get together at least once a year, and the benefits of this collaboration are huge.

The priority is to allow people to collaborate while maintaining their independent brand. There’s so much to learn, and we have a unique opportunity to just talk to other founders and experts in their teams about topics like adding new features, pricing strategies, and much more.

Hopefully, the end result will be better outcomes for the team, the product, and ultimately for your customers.

- What are the biggest challenges that you see for a centralized support system and how is it possible to tackle them?

I think what’s hard is we all have different products and different users, and the challenge is trying to find something that would apply to everyone.

So I think that what we can do is just focus on the customer and how we can do our best job for them with our products and our support. As an organization, we can continue looking for the crossovers and the parallels between our brands under the saas.group umbrella.

As we grow, I think that those matches will just continue to increase. And we’ll naturally find the resources in certain areas that apply across brands.

At the moment, the brands are set up differently, sometimes without the exact same roles having the same responsibilities. In smaller teams, you have people wearing many hats and they may be performing support on top of other responsibilities. I think as we grow, we’ll understand these things a bit better and find the resources to really tackle these challenges and help our brands and their teams grow together and individually.

- What would be your best advice to founders, to teams who are just at the beginning, and just starting to think about building their first customer support team?

As I mentioned before, I think number one would be looking for a culture match. Does somebody share the vision of your organization? Do you feel like it’s a good fit and they’re going to perpetuate and treat your customers the way you do or the way they historically have been treated by your brand?

Leading by example is the key here. You show your customer support how you want your company to be viewed in terms of a certain tone or responsiveness.

Once you have your agents, it’s important to continue to really make an effort to identify their strengths and their interests. Maybe they have a knack for reporting or are great on the creative side. Maybe it’s something that isn’t necessarily your strength or capacity, but spend some effort and time to try and learn that about the people on your team because you never know how you can contribute to their professional growth. And in turn, they can contribute to the growth of your brands.

And then I would say just have trust and give enough autonomy to your people to make decisions. You want to be able to trust the people you are leaving your customers in the hands of, right? That will help foster great relationships inside the organization, growth opportunities, and a feeling of ownership for your brand.

You want people who believe in your vision and are working towards the same goal and there is a sense of pride in the work.

Building and maintaining a customer-centric approach to support is not just about addressing issues; it’s about fostering relationships and driving success for both customers and brands alike. With a centralized support system, saas.group aims to amplify collaboration, share knowledge, and ultimately enhance the customer experience across all its brands.

Check out our website’s blog page to learn more about the initiatives we explore at saas.group to drive growth and take our brands to the next level.

If our values speak to you and resonate with how you do business, get in touch. Discuss your options with our M&A team: Dirk (dirk@saas.group) or Pavel (pavel@saas.group). Learn more about how we grow acquired brands on our blog and podcast pages.

The post Building a centralized customer support system at saas.group appeared first on saas.group.

]]>